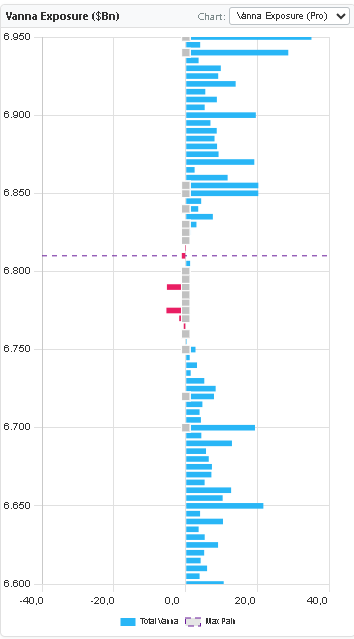

Vanna measures how much an option's delta changes when implied volatility (IV) changes. In mathematical terms: ∂Δ/∂σ — the partial derivative of delta with respect to volatility.

For market makers hedging their options books, Vanna creates a problem: when VIX moves (implied volatility changes), their delta changes even if price doesn't move. They must re-hedge — creating directional flows in the underlying that are entirely driven by volatility, not price action.

🌊 Vanna in plain terms

When VIX drops sharply (implied vol crushes), out-of-the-money call deltas increase. Dealers holding short calls must buy more of the underlying to re-hedge. This creates a vol-crush rally — price rises not because of bullish news, but because volatility falling forces mechanical buying. This is one of the most common "no catalyst" rallies in the market.

- Positive Vanna flow: VIX drops → dealers buy the underlying → price rises

- Negative Vanna flow: VIX spikes → dealers sell the underlying → price falls

- Most powerful when large OTM option positions exist

- Often explains "mystery rallies" after volatility compression