Index futures (ES, NQ, RTY) don't trade in a vacuum. The S&P 500 options market carries over $80 billion in gross gamma. When SPX moves 1%, options market makers must execute billions in offsetting trades in the underlying — which means in ES futures.

This dealer hedging is mechanical and non-discretionary. It follows mathematical rules that don't care about chart patterns, news, or market sentiment. The result: specific price levels where large amounts of automated buying or selling will occur.

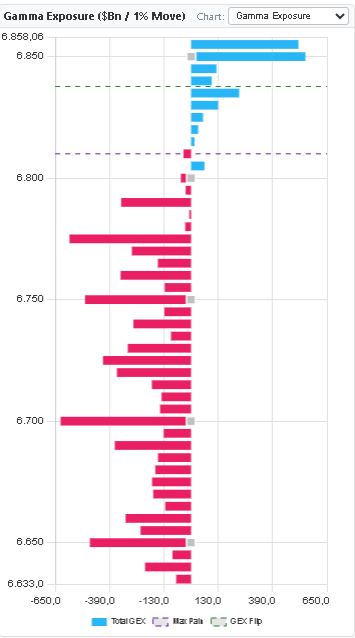

Futures traders who ignore this data are competing without knowing where the $80B elephant in the room is going to step next.

The core insight: You don't trade options. But the people who do trade options force dealers to trade futures to hedge. That dealer activity creates the support, resistance, and momentum you see on your ES/NQ chart every day.