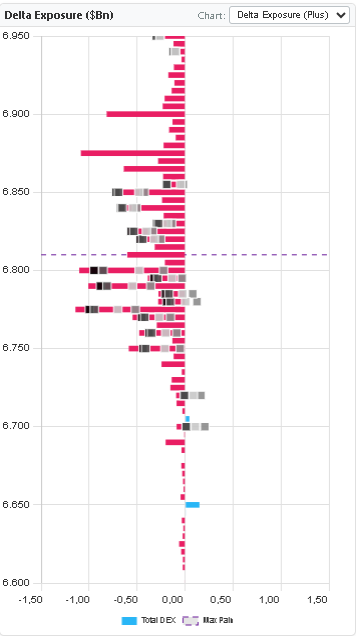

Delta measures how much an option's value changes for a $1 move in the underlying. A call option has a delta between 0 and +1. A put option has a delta between -1 and 0. Delta Exposure (DEX) aggregates the total delta across all options positions that market makers hold.

Unlike gamma (which is symmetric and about speed of hedging), delta tells us the directional bias of dealer positioning. A large negative total delta means dealers are net short the market — they're holding more put exposure than call exposure, and the underlying itself is their hedge on the long side.

Simple analogy: If dealers are short $5 billion in delta (net short the market), they hold $5 billion worth of the underlying as a hedge. Any price move that changes that delta requires them to adjust that hedge — creating directional flows that move price.

- Call delta: 0 to +1 (dealers short calls = dealers long underlying to hedge)

- Put delta: -1 to 0 (dealers short puts = dealers short underlying to hedge)

- Total dealer delta is often negative in put-heavy markets

- Delta exposure reveals the structural directional tilt of the market