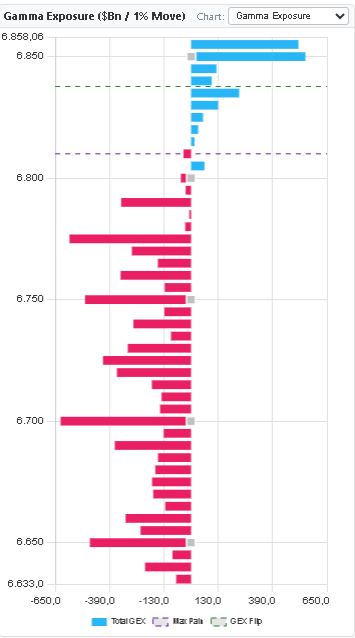

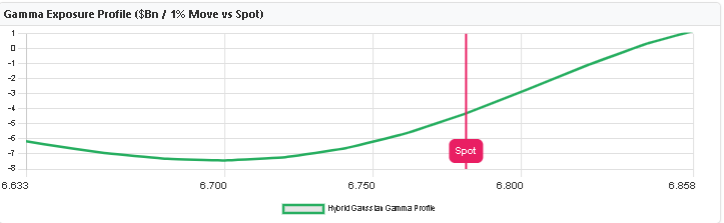

Gamma Exposure (GEX) measures the aggregate gamma that options market makers carry across all strikes and expirations. More precisely, it quantifies how much dealers' total delta changes for every 1% move in the underlying price.

When GEX is high at a specific price level, dealers must execute large buy or sell orders in the underlying to stay delta-neutral. This mechanical hedging is not a choice — it follows mathematical rules. The result is predictable, structural buying and selling pressure at those levels.

The GEX Formula:

GEX = Option Gamma × Open Interest × Contract Size × Spot Price² × 0.01

A positive number means dealers are net long gamma (stabilizing). A negative number means dealers are net short gamma (amplifying).

GEX = Option Gamma × Open Interest × Contract Size × Spot Price² × 0.01

A positive number means dealers are net long gamma (stabilizing). A negative number means dealers are net short gamma (amplifying).

- Market makers always aim to stay delta-neutral

- High GEX levels require aggressive hedging activity

- Hedging flows create magnetism at key price levels

- GEX sign (+ or −) determines market behavior regime